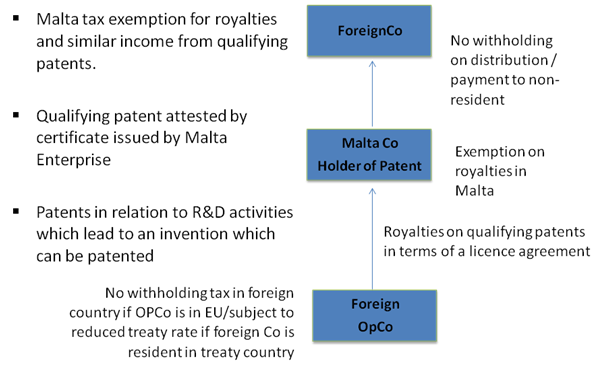

0% Tax on Royalties – ‘Patent Box’

Applies on royalties derived from patents in respect of inventions. The IP must be the result of research and development activities that may have been performed anywhere in the world, leading to an invention which has then been patented anywhere in the world.

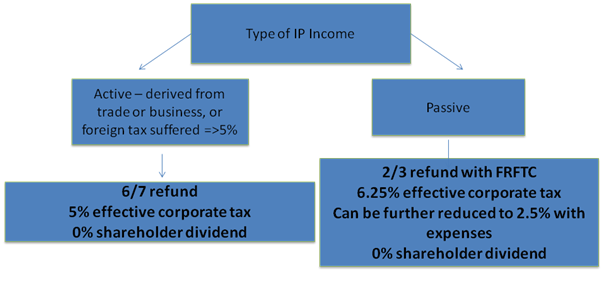

Other royalties derived from non-exempt IP (i.e. trademarks, domains, software)

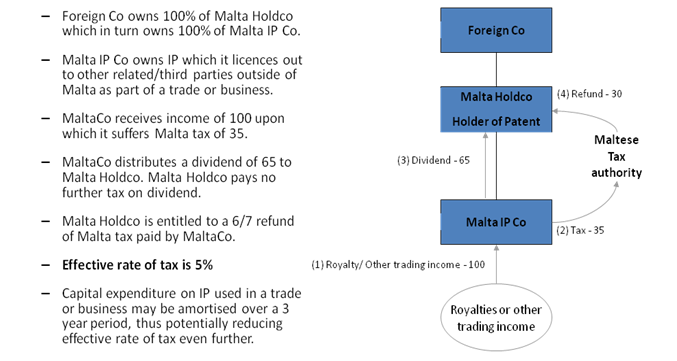

IP Company trading in royalties

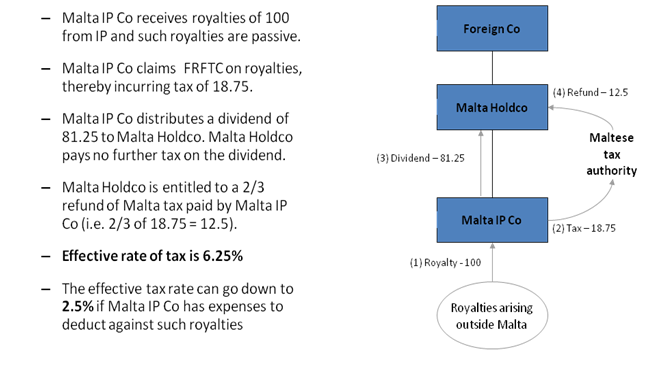

IP Company receiving passive royalties

Entry and exit strategies

Step-up value of IP from cost to market value on entry

No exit taxes – possibilities to transfer residence or domicile outside Malta without triggering Malta tax.